2014 was a great year to be invested in REITs (and other stocks). If you bought the sector by going long IYR (iShares U.S. Real Estate ETF) in January and held on until the end of December you would have realized returns over 20%. If you started that same strategy this year, however, you would be barely breaking even.

The IYR ETF holds a basket of 113 REITs covering a range of strategies and asset types. Its largest holding, at approximately 7% of the portfolio, is Simon Property Group (SPG). The top 18 holdings represent 50% of the portfolio value; the remaining 92 securities provide for the rest of the portfolio. The portfolio covers the entire real estate investing spectrum. Simon Property Group (SPG) owns and operates retail shopping properties; American Tower REIT (AMT) owns and operates cell towers; Public Storage REIT (PSA) is in the self-storage business; Equity Residential REIT (EQR) is a residential apartment landlord. Other holdings cover the hotel, office, industrial and mortgage niches.

Within these 113 holdings there have been a wide range of returns over the last few months. There is a roughly 50/50 split between gainers and losers in the portfolio; only 60 stocks have managed to show a gain for the year. Of these, only 46 have outperformed the S&P 500.

The best performing stock by a wide margin, up over 20%, has been Gaming and Leisure Properties REIT (GLPI). GLPI’s stellar performance is worth noting and may be a harbinger of things to come if more casino operators decided to create REIT spinoffs.

| Top 5 Performers | YTD Change |

| GAMING AND LEISURE PROPERTIES REIT (GLPI) | 24.97% |

| HOWARD HUGHES CORP. (HHC) | 16.54% |

| XENIA HOTELS RESORTS REIT INC (XHR) | 15.77% |

| EXTRA SPACE STORAGE INC. (EXR) | 15.08% |

| RYMAN HOSPITALITY PROPERTIES REIT (RHP) | 14.50% |

The worst performers are clustered in a tight grouping of positions which have sunk 11% to 12% for the year. Two members of this ignominious grouping are PCH (Potlatch Corp.) and WY (Weyerhaeuser REIT). Both of these firms primarily invest in timberlands and their decline is no surprise given the collapse in lumber prices this year. The NAHB’s survey of Framing Lumber Prices shows a steady decline in lumber prices from the very beginning of 2015.

| Bottom 5 Performers | YTD Change |

| POTLATCH CORP. (PCH) | -11.02% |

| WEYERHAEUSER REIT (WY) | -11.04% |

| COUSINS PROPERTIES REIT INC (CUZ) | -11.20% |

| HOST HOTELS & RESORTS REIT INC (HST) | -12.28% |

| LEXINGTON REALTY TRUST REIT (LXP) | -12.55% |

Another position down over 12% is HST (Host Hotels and Resorts REIT Inc) who you may recognize through their Marriot and Hyatt brands (amongst others). Unfortunately for Host its poor performance is unique amongst the hospitality sector. For example, (XHR) (Xenia Hotels Resorts REIT Inc) and RHP (Ryman Hospitality Properties REIT) are each up approximately 15% this year.

The worst performer in this portfolio is LXP (Lexington Realty Trust REIT), a net-lease REIT. As covered in other articles, this company appears to be suffering from problems of its own making and is not necessarily representative of the net-lease sector.

If we step-back and take a macro, sector-based look at the state of the market we will notice that 8 market sectors (as represented by their iShares ETFs) have outperformed IYR. Only one sector (financials) has done worse than real estate this year.

| Market Sector | YTD Change |

| Real Estate (IYR) | 1.12% |

| Healthcare (IYH) | 9.73% |

| Telecommunications (IYZ) | 8.60% |

| Consumer Services (IYC) | 6.76% |

| Technology (IYW) | 4.15% |

| Energy (IYE) | 3.82% |

| Consumer Goods (IYK) | 3.29% |

| Industrials (IYJ) | 2.81% |

| Basic Materials (IYM) | 2.20% |

| Financial (IYF) | -0.31% |

The overall weakness of the IYR ETF, with 53 stocks losing money YTD, indicates a decided investor rotation out of the real estate sector. This weakness stems from two sources. The first source, which is exogenous to real estate is the looming rise in interest rates. With their large dividend payouts REITs are sensitive to changes in relative yields as compared to other investments, particularly those in the fixed-income sector. Related to this is the recognition of REITs dependence on leverage (i.e. mortgages) to finance their acquisitions. As their loan payments reset, either because they are floating-rate instruments or they are due for refinancing, each REIT’s debt service will become more expensive thus reducing the cash available for distribution to shareholders.

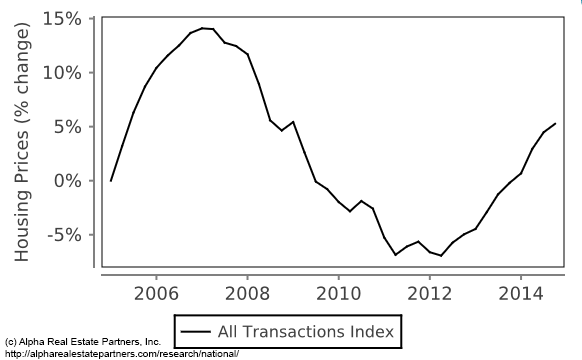

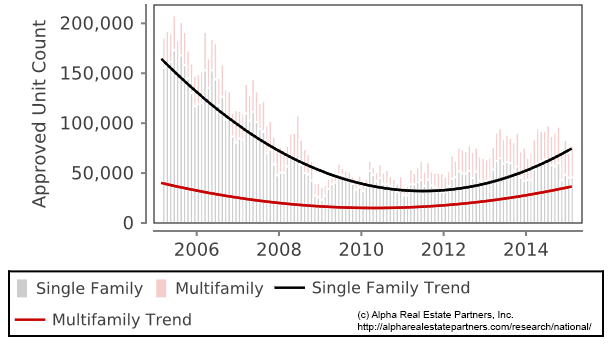

A further source of weakness, endogenous to the business, is the concern that real estate prices have become overheated and we are reaching the peak of this real estate cycle. Nationwide housing prices and residential building permits have erased the losses made in the aftermath of the 2008 financial crisis (despite continued weakness in the labor market).

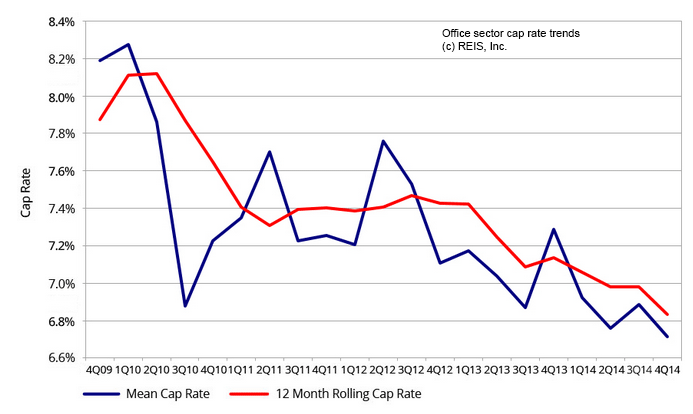

Similarly in other real estate sectors we see yields (referred to as “cap rates” in real estate parlance) falling sharply over the last few years. Since a fall in yields is synonymous with a rise in prices many have been led to ask if REITs are overpaying for their recent acquisitions.

Despite the weak performance of the IYR ETF individual stocks in its portfolio have performed remarkably well. Going-forward we believe that investors will need to build the real estate component of their balanced portfolios by identifying strong names in the sector. The free ride of 2014 is over; we now need to do our homework to find the right investments instead of relying on the strength of the entire sector to carry us through.

So where do we go from here? One strategy is to inspect the components of IYR and see if there are any commonalities amongst the top-performing stocks. Two of the top ten, Lamar Advertising Company (LAMR) and Outfront Media Inc (OUT) are advertising firms (primarily providing billboards); their future business is more closely tied to growth in the US economy than to the real estate industry. Another interesting top-ten is CBRE Group Inc. (CBG). CBRE is one of the leading brokerage and real estate services companies in the US. As long as there are property owners buying, selling and managing properties CBRE will continue to make money.

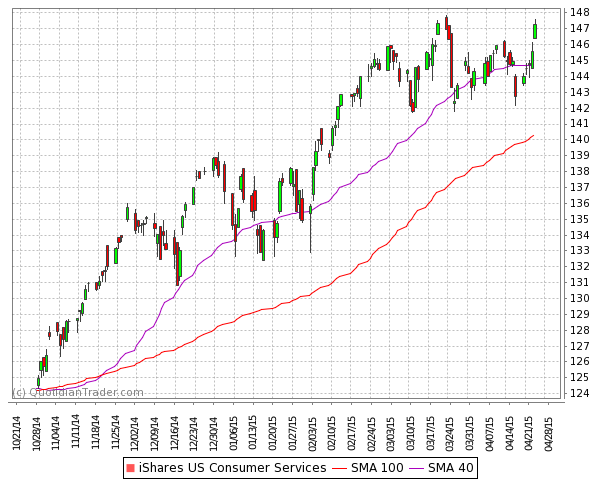

And, perhaps, it’s time to look into investing in other, less interest rate sensitive, sectors. Consumer services, as represented by IYC, has held up well this year and should continue to show strongly if the domestic economy continues to grow.

The healthcare sector, as represented by IYH, has been rising strongly as well. This author wonders if continued strength in healthcare will eventually show itself in the stocks of healthcare related REITS, such as Health Care REIT Inc. (HCN), Healthcare Realty Trust Inc. (HR) and Healthcare Trusts of America REIT (HTA). These three stocks are down for the year (though not by much) but we have noticed that there is strong demand for healthcare related properties (hospitals, doctors offices, etc.) amongst non-institutional buyers. This investor demand is driven by steadily rising tenant demand for medical office space as medical practices consolidate and upgrade facilities in reaction both to Obamacare and the ageing of baby boomers. This investor and user demand should translate into higher rents for the properties held by these REITs which should ultimately result in higher income to these REITs.

This article was originally published April 27, 2015 at Seeking Alpha.

Download the data used in this analysis.